Introduction, Overview of Operations, And Brief History: The company I will be focusing on in this article is Strattec Security Corporation (STRT, Financial). Strattec is a nano cap with a current market cap around $75 million, and it is in the very boring and shunned automotive parts industry. The company has expanded to become a worldwide auto parts supplier through its various joint ventures and alliances.

The company makes and sells various automotive parts such as: keys with radio frequency identification technology, bladeless electronic keys, ignition lock housings, trunk latches, lift gate latches, tailgate latches, hood latches and side door latches. With its acquisition of Delphi Corporation's Power Products in 2009 it is now also supplying power access devices for sliding side doors, lift gates and trunk lids.

In 2001 Strattec formed an alliance with Witte-Velbert Gmbh. The alliance allowed Strattec to sell Witte's products in the US, and allowed Witte to sell Strattec's products in Europe. In 2006 the alliance expanded to include ADAC plastics and a joint venture with all three companies owning 33% was formed called VAST or Vehicle Access Systems Technology. ADAC makes such products as door handles. The VAST Alliance has helped Strattec become a worldwide auto parts supplier as the alliance allows all companies involved to market and sell each other’s products in various jurisdictions around the world including in the U.S., Europe, Brazil, China, Japan, and Korea. The VAST Alliance should have its first profitable year as a company this year which would help Strattec's bottom line. Full complement of VAST's products can be viewed here.

Picture taken from ADAC Plastics which shows how the VAST Alliance is structured.

ADAC and Strattec have formed a separate company, ADAC-Strattec de Mexico, ASdM, whose operations are in Mexico due to cheaper labor prices, where the two companies separate expertise are combined to manufacture some of the above products for sale. In Strattec's fiscal years ending 2012 and 2011, ASdM was profitable and represented $31.0 and $25.2 million, respectively of Strattec's consolidated net sales.

With the help of VAST and its other joint ventures, Strattec's export sales have risen to 37% of total sales which amounts to $107 million. In 2001 exports only accounted for 14% of its sales which amounted to $29 million, which illustrates Strattec's worldwide growth since then.

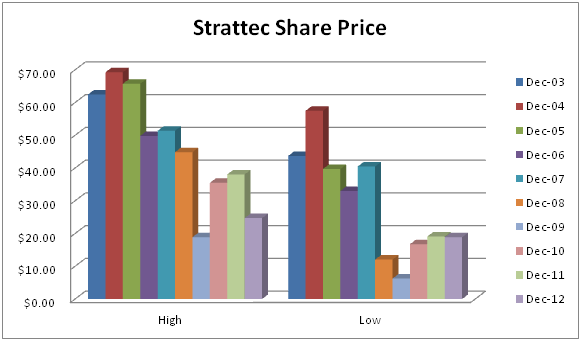

During the recession three of Strattec's biggest buyers filed for bankruptcy protection, and the overall auto industry went to the brink of death before being saved by the U.S. federal government. Because Strattec's major buyers were having so many problems, it also faced some very serious problems and had its only unprofitable year in 2009, lost more than $40 per share in value during the recession, about two-third of its share price in total, and its share price has not recovered since.

Since that time Strattec restructured, improved its operations and expanded its product lines, and signed various joint venture and alliance agreements which have allowed the company to become a worldwide auto parts supplier. The restructuring, expanded product lines, and worldwide operations have helped Strattec become a more diversified auto parts manufacturer and has grown its sales and margins in the ensuing years. With the help of VAST and its other joint ventures Strattec is a truly worldwide company with operations now in the U.S., Europe, Brazil, China, Japan, Korea, Canada and Mexico.

Strattec was spun off from Briggs & Stratton in 1995 as an independent company. After Strattec was spun off from Briggs & Stratton, and through most of its entire history, it enjoyed massive market share of over 60% in the U.S. and a 20% market share of the world's vehicle lock and key operations. With its huge hold of the market the company was able to dictate high prices to its buyers which enabled the company to enjoy a competitive advantage for a long period of time.

However, shortly after Strattec was spun off there were massive changes in the lock and key industry which deteriorated the company’s market share and competitive advantages. Due to Strattec's managements excellent foresight and planning, it was well prepared for the change from basic locks and keys and the diminishing of the amount of locks and keys needed per vehicle, and has transitioned into the electronic key arena as well as expanding its operations into various fields though its partnerships with the VAST Alliance including: Door handles, power doors, trunk latches, lift gate latches, tailgate latches, hood latches, side door latches, ignition lock housings, sliding side doors, lift gates and trunk lids. Since Strattec's restructuring during the Great Recession, along with its VAST Alliance and other joint ventures, improved operations, and expanded product lines, Strattec's sales and margins have both been growing and improving. The trend of growing sales and margins should continue unless another recession hits.

Excellent Management

Due to the excellent leadership of Harold Stratton II, former CEO and current chairman, current CEO and board member Frank Karecji, and the other members of Strattec's management team and board of directors, it has been able to adjust its original lock and key operations and changed massively to become a truly worldwide auto parts supplier with the products listed above.

Normally I do not talk much about management in my articles because I usually deem management to be either average or sub-par and as Charlie Munger says, I want the business to be simple enough to be able to be run by the proverbial "idiot nephew." So management is generally not a factor in my analysis unless they are doing things that bother me quite a bit.

In this case I wanted to point out that I believe Strattec's management to be excellent, and I think that will continue now that Stratton has transitioned out of the day-to-day operations and handed them to Karecji. For the full view of why I believe Strattec's management to be excellent I recommend reading its annual reports from 1999 to the present, and to get a glimpse of the obstacles management has helped the company overcome to become an even stronger company. Here is a profile of Karecji, Strattec's new CEO, from 2010, right after he joined the company.

For those who do not want to read all that information I will list a few positive developments from management in recent years that I have not already talked about.

Competitors

The company faces stiff competition from the following three companies.

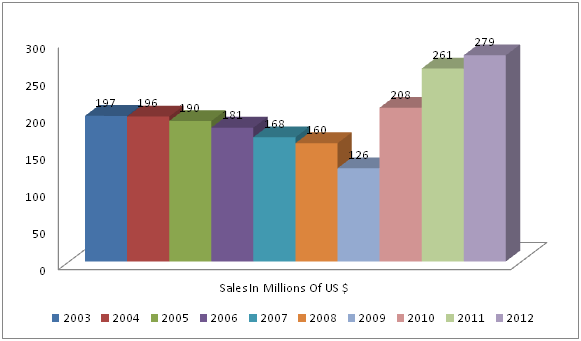

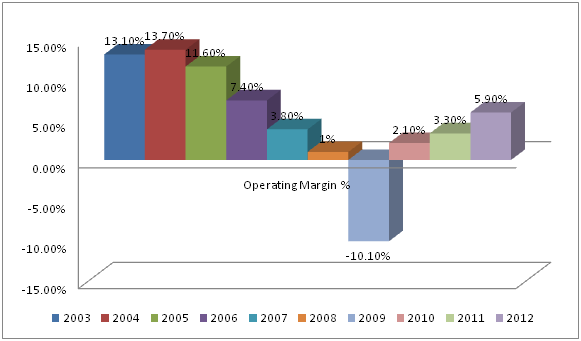

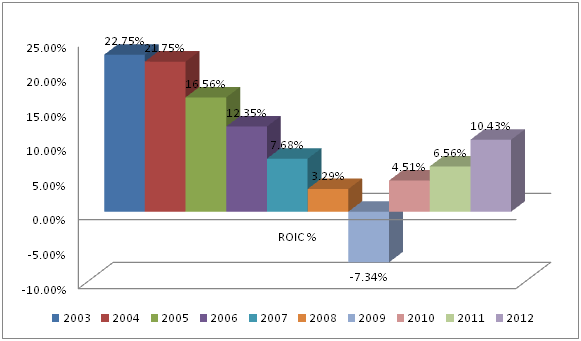

Strattec's Margins

All numbers were taken from Morningstar or Yahoo Finance unless otherwise noted. Final four debt calculations are including total debt and obligations.

Margin Conclusion Thoughts

As you can see in the above graphs, Strattec's share price has not improved as its operations and sales have. The last year Strattec had comparable margins to what it had this year is 2006, when Strattec was selling for between $33 and $50 a share. As I found after doing my valuations, which I will show below, Strattec should be selling somewhere in that range now. Sales are actually almost $100 million more than they were in 2006, and margins should continue to improve as Strattec's now worldwide operations and expanded product lines become more efficient.

Valuations

These valuations were done by me, using my estimates and are not a recommendation to buy stock in any of the companies mentioned. Do your own homework.

Valuations were done using the 2012 10-K and 2013 first quarter 10-Q. All numbers are in millions of U.S. dollars, except per share information, unless otherwise noted.

Low Estimate Of Intrinsic Value

Base Estimate Of Intrinsic Value

Number of shares are 3.3

Reproduction Value

Cash and cash equivalents are $12.94

Short term investments are $0

Total current liabilities are $57.8

Number of shares are $3.3

Cash and cash equivalents + short-term investments - total current liabilities=12.94-57.8=-44.86

5x, 8x, 11x and 14x EBIT + cash and cash equivalents + short-term investments:

I discounted the cash a bit in the above valuations because about 55% of Strattec's cash is in Mexico, so if Strattec wanted to bring the funds to the U.S. it would have to pay taxes on that portion of cash.

With all of the above taken into account, I think that the absolute minimum Strattec should be selling for is $29.43 per share which assumes that Strattec's EBIT margin will revert to its three-year average. It is currently selling for around $23.50 per share. I think that Strattec's true intrinsic value is somewhere between $35 and $45 per share. None of that is even taking into account that its sales and margins should continue to grow, which would also grow the company's intrinsic value.

The company does face some headwinds to future growth as I outline above. The biggest ones are that Strattec has to compete with various bigger companies, and I do not see any kind of long-term sustainable competitive advantages within the company.

Normally I would want some kind of sustainable competitive advantage within a company that I am buying as a long-term value hold, but at current valuations, with Strattec's good and rising margins and other factors listed throughout the article, the risk/reward is in my favor by a substantial margin and I have already bought shares for my personal account and the accounts I manage, making this only the fourth company I have bought into this year.

The company makes and sells various automotive parts such as: keys with radio frequency identification technology, bladeless electronic keys, ignition lock housings, trunk latches, lift gate latches, tailgate latches, hood latches and side door latches. With its acquisition of Delphi Corporation's Power Products in 2009 it is now also supplying power access devices for sliding side doors, lift gates and trunk lids.

In 2001 Strattec formed an alliance with Witte-Velbert Gmbh. The alliance allowed Strattec to sell Witte's products in the US, and allowed Witte to sell Strattec's products in Europe. In 2006 the alliance expanded to include ADAC plastics and a joint venture with all three companies owning 33% was formed called VAST or Vehicle Access Systems Technology. ADAC makes such products as door handles. The VAST Alliance has helped Strattec become a worldwide auto parts supplier as the alliance allows all companies involved to market and sell each other’s products in various jurisdictions around the world including in the U.S., Europe, Brazil, China, Japan, and Korea. The VAST Alliance should have its first profitable year as a company this year which would help Strattec's bottom line. Full complement of VAST's products can be viewed here.

Picture taken from ADAC Plastics which shows how the VAST Alliance is structured.

ADAC and Strattec have formed a separate company, ADAC-Strattec de Mexico, ASdM, whose operations are in Mexico due to cheaper labor prices, where the two companies separate expertise are combined to manufacture some of the above products for sale. In Strattec's fiscal years ending 2012 and 2011, ASdM was profitable and represented $31.0 and $25.2 million, respectively of Strattec's consolidated net sales.

With the help of VAST and its other joint ventures, Strattec's export sales have risen to 37% of total sales which amounts to $107 million. In 2001 exports only accounted for 14% of its sales which amounted to $29 million, which illustrates Strattec's worldwide growth since then.

During the recession three of Strattec's biggest buyers filed for bankruptcy protection, and the overall auto industry went to the brink of death before being saved by the U.S. federal government. Because Strattec's major buyers were having so many problems, it also faced some very serious problems and had its only unprofitable year in 2009, lost more than $40 per share in value during the recession, about two-third of its share price in total, and its share price has not recovered since.

Since that time Strattec restructured, improved its operations and expanded its product lines, and signed various joint venture and alliance agreements which have allowed the company to become a worldwide auto parts supplier. The restructuring, expanded product lines, and worldwide operations have helped Strattec become a more diversified auto parts manufacturer and has grown its sales and margins in the ensuing years. With the help of VAST and its other joint ventures Strattec is a truly worldwide company with operations now in the U.S., Europe, Brazil, China, Japan, Korea, Canada and Mexico.

Strattec was spun off from Briggs & Stratton in 1995 as an independent company. After Strattec was spun off from Briggs & Stratton, and through most of its entire history, it enjoyed massive market share of over 60% in the U.S. and a 20% market share of the world's vehicle lock and key operations. With its huge hold of the market the company was able to dictate high prices to its buyers which enabled the company to enjoy a competitive advantage for a long period of time.

However, shortly after Strattec was spun off there were massive changes in the lock and key industry which deteriorated the company’s market share and competitive advantages. Due to Strattec's managements excellent foresight and planning, it was well prepared for the change from basic locks and keys and the diminishing of the amount of locks and keys needed per vehicle, and has transitioned into the electronic key arena as well as expanding its operations into various fields though its partnerships with the VAST Alliance including: Door handles, power doors, trunk latches, lift gate latches, tailgate latches, hood latches, side door latches, ignition lock housings, sliding side doors, lift gates and trunk lids. Since Strattec's restructuring during the Great Recession, along with its VAST Alliance and other joint ventures, improved operations, and expanded product lines, Strattec's sales and margins have both been growing and improving. The trend of growing sales and margins should continue unless another recession hits.

Excellent Management

Due to the excellent leadership of Harold Stratton II, former CEO and current chairman, current CEO and board member Frank Karecji, and the other members of Strattec's management team and board of directors, it has been able to adjust its original lock and key operations and changed massively to become a truly worldwide auto parts supplier with the products listed above.

Normally I do not talk much about management in my articles because I usually deem management to be either average or sub-par and as Charlie Munger says, I want the business to be simple enough to be able to be run by the proverbial "idiot nephew." So management is generally not a factor in my analysis unless they are doing things that bother me quite a bit.

In this case I wanted to point out that I believe Strattec's management to be excellent, and I think that will continue now that Stratton has transitioned out of the day-to-day operations and handed them to Karecji. For the full view of why I believe Strattec's management to be excellent I recommend reading its annual reports from 1999 to the present, and to get a glimpse of the obstacles management has helped the company overcome to become an even stronger company. Here is a profile of Karecji, Strattec's new CEO, from 2010, right after he joined the company.

For those who do not want to read all that information I will list a few positive developments from management in recent years that I have not already talked about.

- Strattec has bought back and reduced its shares outstanding by 3.66 million, or more than 50% of its original shares outstanding after being spun off, at a cost of approximately $136 million.

- Most purchases have been at good prices to do buy backs. I think now would be an even better time to buy back more shares (Strattec management has authorization to buy back more shares) because of Strattec's current undervaluation which I will get to later, but I understand that it wants to put money into expanding its operations and product lines.

- Another reason Strattec has not bought any shares back in the past couple years is it has been concentrating on reinstating its dividend and expanding its VAST Alliance operations. The company currently only has 3.3 million shares left that are outstanding.

- Management compensation is fair and straightforward, which is another positive for management.

- GAMCO Investors: Collectively Mario Gabelli's Funds own 18.6% of Strattec.

- T. Rowe Price and Associates through its Small Cap and Small Value funds own 15.5% of Strattec.

- FMR-Fidelity Management and Research Company own 12.2% of Strattec.

- Vanguard Horizon Funds own 6.2% of Strattec.

- Dimensional Fund Advisors, a small cap value fund, owns 5.8% of Strattec.

- Insiders own 7.82% according to Reuters.

- The above insiders and funds own a combined 66.12% of Strattec which partially explains why there is a very low average daily trading volume of around 2,000 shares per day in the stock.

Competitors

The company faces stiff competition from the following three companies.

- Magna International (MGA, Financial): I talked about Magna a bit in my Core Molding Technologies (CMT, Financial) article and how I did not think that Magna was a major threat to CMT's area of operations. The story as it pertains to Strattec's operations is different, however. Magna competes with Strattec in several of its product lines including the power access area and Magna appears to be a major player in those areas. In 2009 Strattec bought the Power Access portion of Delphi's business segment after it went bankrupt and renamed the unit Strattec Power Access. For fiscal years ending 2012 and 2011, Strattec Power Access was profitable and represented $62.7 and $62.8 million, respectively, of Strattec's consolidated net sales. Just for comparison, Magna did $1.2 billion in sales in its closure systems (power access) business alone in 2011. Magna could present a problem for future growth of Strattec's product lines as it will have to compete vigorously on price and quality for contracts. It could also present a potential opportunity as with CMT; I could see Magna possibly buying out Strattec to expand its operations into more product fields. This makes further sense since Strattec is such a small company in comparison to Magna and a more than $11 billion marke-cap company.

- Huf huelsbeck & fuerst: Huf and its various subsidiaries including Huf North America is a privately held company with operations worldwide and whose product lines compete directly with Strattec's on almost every product around the world. This company presents the same problem as Magna does to Strattec, but the same potential buy out opportunity exists as well.

- Tokai Rika: This is a Japanese publicly traded company who competes directly with Strattec on several products and who also has operations around the world. Tokai Rika, like the two companies mentioned before, also dwarfs Strattec in size, which could present problems to Strattec's growth.

Strattec's Margins

All numbers were taken from Morningstar or Yahoo Finance unless otherwise noted. Final four debt calculations are including total debt and obligations.

| Gross Margin TTM | 18.50% |

| Gross Margin 5 Year Average | 15.32% |

| Gross Margin 10 Year Average | 18.25% |

| Op Margin TTM | 6.20% |

| Op Margin 5 Year Average | 0.44% |

| Op Margin 10 Year Average | 5.18% |

| ROE TTM | 12.11% |

| ROE 5 Year Average | 3.59% |

| ROE 10 Year Average | 9.91% |

| ROIC TTM | 11.90% |

| ROIC 5 Year Average | 3.49% |

| ROIC 10 Year Average | 9.85% |

| My ROIC Calculation With Goodwill | 25.90% |

| My ROIC Calculation With Goodwill If EBIT% Reverts to 3 Yr Avg | 15.41% |

| My ROIC Calculation Without Goodwill | 25.82% |

| My ROIC Calculation Without Goodwill If EBIT% Reverts to 3 Yr Avg | 15.37% |

| FCF/Sales TTM | 2.25% |

| FCF/Sales 5 Year Average | -3.49% |

| FCF/Sales 10 Year Average | 1.71% |

| Cash Conversion Cycle TTM | 54.43 days |

| Cash Conversion Cycle 5 Year Average | 48.97 days |

| Cash Conversion Cycle 10 Year Average | 42.42 days |

| P/B Current | 0.9 |

| Insider Ownership Current | 7.82% |

| My EV/EBIT If EBIT% Reverts to 3 Yr Avg | 5.77 |

| My EV/EBIT Current Unadjusted | 3.43 |

| My TEV/EBIT If EBIT% Reverts to 3 Yr Avg | 8.09 |

| My TEV/EBIT Current Unadjusted | 4.81 |

| Working Capital TTM | $46 million |

| Working Capital 5 Yr Avg | $48.6 million |

| Working Capital 10 Yr Avg | $60 million |

| Book Value Per Share Current | $25.25 |

| Book Value Per Share 5 Yr Avg | $24.54 |

| Book Value Per Share 10 Yr Avg | $24.78 |

| Float Score Current | 0.53 |

| Float Intensity | 0.77 |

| Debt Comparisons: | |

| Total Debt as a % of Balance Sheet TTM | 0.88% |

| Total Debt as a % of Balance Sheet 5 year Average | 0.66% |

| Total debt as a % of Balance Sheet 10 year Average | 0.33% |

| Current Assets to Current Liabilities | 1.79 |

| Total Debt to Equity | 45% |

| Total Debt to Total Assets | 22% |

| Total Obligations and Debt/EBIT | 2.1 |

| Total Obligations and Debt/EBIT If EBIT Reverts To 3 Yr Avg | 3.53 |

Margin Conclusion Thoughts

- The very first thing that pops out from the above margins is that across the board Strattec has improved its margins, sometimes by multiple percentage points, in comparison to its 5-year and 10-year averages. Looks like the restructuring that took place during the recession, the various joint ventures including the VAST Alliance, and branching out to new product lines have helped the company immensely. Improvements in operating margin, ROE and ROIC have all been especially impressive.

- My ROIC calculations make the company look even better as even if Strattec were to revert to its three-year average EBIT, which I don't think it will unless another recession happens, I am estimating it to have an ROIC of 15.37% without goodwill. If Strattec is able to keep up its EBIT margin to current levels I estimate that without goodwill its ROIC is 25.82%, an astounding ROIC margin.

- Also positive as it pertains to ROIC is that in Strattec's case it is not being artificially inflated by high amounts of debt.

- The cash conversion cycle has gotten worse over the years, meaning less efficiency in the company, which I generally do not like. That is to be expected in a company that has expanded operations overseas though, so no red flag there.

- Its P/B ratio at 0.9 is less than half that of its industry P/B at 2 which means that at least on a relative basis Strattec is undervalued in comparison to its industry.

- My current unadjusted EV/EBIT ratio estimate for Strattec is 3.43. Unadjusted TEV/EBIT estimate is 4.81. Generally I like to buy companies selling at an EV/EBIT ratio of 8 or less so again Strattec appears to be undervalued.

- Even if Strattec's EBIT margin were to revert back to its three-year average, which as above I do not think it will do unless there is another recession, its EV/EBIT ratio is 5.77 and TEV/EBIT is 8.09, again undervalued or about fairly valued at worst.

- Book value per share has grown slightly over time, and should grow further with its improved operations.

- The company has minimal debt and even if we include its total contractual obligations and debt its total obligations/EBIT ratio is a paltry 2.1. This is much improved from some of the other companies I have evaluated, and its current total debt and obligations should be nothing to worry about going forward.

As you can see in the above graphs, Strattec's share price has not improved as its operations and sales have. The last year Strattec had comparable margins to what it had this year is 2006, when Strattec was selling for between $33 and $50 a share. As I found after doing my valuations, which I will show below, Strattec should be selling somewhere in that range now. Sales are actually almost $100 million more than they were in 2006, and margins should continue to improve as Strattec's now worldwide operations and expanded product lines become more efficient.

Valuations

These valuations were done by me, using my estimates and are not a recommendation to buy stock in any of the companies mentioned. Do your own homework.

Valuations were done using the 2012 10-K and 2013 first quarter 10-Q. All numbers are in millions of U.S. dollars, except per share information, unless otherwise noted.

Low Estimate Of Intrinsic Value

| Numbers: | ||||

| Revenue: | 284 | |||

| Multiplied By: | ||||

| Average 3 year EBIT %: | 3.77% | |||

| Equals: | ||||

| Estimated EBIT of: | 10.71 | |||

| Multiplied By: | ||||

| Assumed Fair Value Multiple of EBIT: | 8X | |||

| Equals: | ||||

| Estimated Fair Enterprise Value of STRT: | 85.68 | |||

| Plus: | ||||

| Cash, Cash Equivalents, and Short Term Investments: | 12.94 | |||

| Minus: | ||||

| Total Debt: | 1.5 | |||

| Equals: | ||||

| Estimated Fair Value of Common Equity: | 97.12 | |||

| Divided By: | ||||

| Number of Shares: | 3.3 | |||

| Equals: | $29.43 per share |

Base Estimate Of Intrinsic Value

| Assets: | Book Value: | Reproduction Value: |

| Current Assets | ||

| Cash And Cash Equivalents | 16.3 | 12.94 |

| Accounts Receivable (Net) | 45.1 | 38.34 |

| Inventories | 25.5 | 15.3 |

| Other Current Assets | 17.1 | 8.6 |

| Total Current Assets | 104 | 75.18 |

| Deferred Income Taxes | 9.7 | 4.9 |

| Investments In Joint Ventures | 8.4 | 4.2 |

| Other Long Term Assets | 0.5 | 0 |

| PP&E Net | 47.6 | 28.6 |

| Total Assets | 170.6 | 112.88 |

Number of shares are 3.3

Reproduction Value

- 112.88/3.3=$34.21 per share.

Cash and cash equivalents are $12.94

Short term investments are $0

Total current liabilities are $57.8

Number of shares are $3.3

Cash and cash equivalents + short-term investments - total current liabilities=12.94-57.8=-44.86

- -44.86/3.3=-$13.59 in net cash per share.

5x, 8x, 11x and 14x EBIT + cash and cash equivalents + short-term investments:

- 5X18=90+12.94=102.94/3.3=$31.19 per share.

- 8X18=144+12.94=156.94/3.3=$47.56 per share.

- 11X18=198+12.94=210.94/3.3=$63.92 per share.

- 14X18=252+12.94=264.94/3.3=$80.29 per share.

I discounted the cash a bit in the above valuations because about 55% of Strattec's cash is in Mexico, so if Strattec wanted to bring the funds to the U.S. it would have to pay taxes on that portion of cash.

- Strattec is undervalued by 23% using my low estimate of value, which assumes that Strattec will revert back to its three-year average EBIT margin, which as I stated above, I do not think will happen unless there is another recession. This is the absolute minimum I think Strattec should be selling for.

- Strattec is undervalued by 33% using my base estimate of intrinsic value on a pure asset reproduction basis.

- Strattec is undervalued by 52% using my high estimate of intrinsic value with EBIT and cash at current levels. Now that Strattec has restructured itself and made itself a worldwide company with expanded product lines and improved operations I actually think that EBIT should rise over time meaning Strattec's intrinsic value could continue to grow and it would become even more undervalued.

- Strattec has excellent management.

- The company is undervalued by every one of my estimates of intrinsic value above and relative valuation estimates such as P/B, EV/EBIT and TEV/EBIT.

- Strattec restructured before and during the recession to cut costs, expand product lines, and became more efficient and less dependent on one single product line.

- Strattec signed joint ventures, and created the VAST Alliance with two other companies that now allow Strattec to compete on a global scale.

- Strattec's margins have improved across the board in comparison to its 5- and 10-year averages and margins should continue to improve.

- Sales have also been improving along with margins.

- Strattec has almost zero debt.

- Strattec management owns just fewer than 8% of the company.

- Most importantly as it pertains to management is that I trust that they have shareholders' best interests in mind.

- Various value and small cap-oriented funds own more than 50% of the company, including Mario Gabelli's funds.

- The VAST Alliance as a company should have its first profitable year this year which should help Strattec's profitability even more.

- My estimates of ROIC show that Strattec is even more profitable than I originally thought while looking at Morningstar's numbers.

- Strattec has a $25 million revolving credit facility if it wants to do any acquisitions, which the new CEO has said he will look into, or the $25 million could be used in an emergency situation if one arises.

- Margins are not artificially inflated by debt so margins show a true picture of how Strattec is running.

- Strattec has drastically reduced its share count in the past decade at good prices to be buying at.

- Strattec is currently authorized to buy back more shares if it chooses to.

- Strattec recently reinstated its quarterly dividend.

- Strattec is highly dependent on only a few customers for its orders as General Motors, Ford and The Chrysler Group combine for 68% of sales.

- Strattec is highly dependent on how well the automotive industry and the overall economy as a whole are doing which can be seen in the above graphs.

- Due to the cyclical nature of Strattec, if there is another recession or major problems in the auto industry again, its sales and profitability will be highly affected.

- The company has some very stiff and much bigger competition. The competition could possibly mean further price cuts on products in Strattec's product lines if some kind of price war starts.

- Due to competition and the overall cost reduction plans put into place by the big automotive companies, Strattec has had to drop prices on its products in recent years.

- At this point I do not see any kind of long-term sustainable competitive advantages within Strattec.

- Since Strattec is very small in comparison to its competitors it could become a potential buy out candidate.

- Strattec's margins should continue to grow which could lead to the unlocking of value.

- The new CEO Frank Karecji has said that he would like to do some kind of acquisition in the short term.

- Strattec is authorized to buy back more shares.

With all of the above taken into account, I think that the absolute minimum Strattec should be selling for is $29.43 per share which assumes that Strattec's EBIT margin will revert to its three-year average. It is currently selling for around $23.50 per share. I think that Strattec's true intrinsic value is somewhere between $35 and $45 per share. None of that is even taking into account that its sales and margins should continue to grow, which would also grow the company's intrinsic value.

The company does face some headwinds to future growth as I outline above. The biggest ones are that Strattec has to compete with various bigger companies, and I do not see any kind of long-term sustainable competitive advantages within the company.

Normally I would want some kind of sustainable competitive advantage within a company that I am buying as a long-term value hold, but at current valuations, with Strattec's good and rising margins and other factors listed throughout the article, the risk/reward is in my favor by a substantial margin and I have already bought shares for my personal account and the accounts I manage, making this only the fourth company I have bought into this year.